Did CAG Rajiv Mehrishi evade tax?

The former finance secretary and current Comptroller and Auditor General received a 2016 income tax notice stating he’d evaded over ₹2.86 crore long-term capital gain.

For two years, Rajiv Mehrishi, sitting Comptroller and Auditor General of India and ex-Finance Secretary, has been battling an income tax assessment order which alleges that he had avoided tax on a land deal at his hometown in Rajasthan. Income tax authorities have not withdrawn the order yet, though Mehrishi claims the issue is pretty much closed.

Income tax documents accessed by Newslaundry reveal that Mehrishi first converted the land-use of a piece of land from agriculture to non-agriculture to get a higher selling price. But once the deal was done, he claimed the profit from it as agricultural income in his tax return and was thereby exempt from being taxed.

The income tax assessment accessed by Newslaundry said: “He (Mehrishi) was managing this transaction in a manner so as to escape from the liability of tax on long-term capital gain.”

In his IT declaration for the year 2014-15, Mehrishi had claimed exempt of income Rs 2,35,69,800 on account of sale of agricultural land. On December 30, 2016, Mehrishi was issued a show cause notice from the Income Tax Department regarding his evasion of over ₹2.86 crore long-term capital gain (LTCG) tax in this particular land deal.

The 1.26-hectare land in question is located at Jaipur’s Gunawata village in a tehsil called Amer. It was sold by Rajiv’s wife Meera—who was given power of attorney by her husband—for a consideration of ₹2,50,000 (the value under Section 50C was taken by the sub-registrar at ₹3,01,23,560 for stamp duty purposes). The land was sold on November 21, 2013.

However, when the IT department went through the sale deed—registered in the office of sub-registrar of Amer—it stated that the land had been converted for non-agriculture purposes as per Section 90A of the Rajasthan Land Revenue Act 1956. An order was also passed by the Jaipur Development Authority (JDA) on December 13, 2012, stating the same.

When the IT department scrutinised Mehrishi’s income tax returns for 2014-15—filed after the requisite due date—it was found that Mehrishi had declared ₹2.35 crore from this land deal as being exempted under agricultural income in his salary. After investigating his tax return, the IT department issued Mehrishi a show cause notice on December 23, 2016, and asked him to explain “why the sale value of the land which was non-agriculture as on date of sale should not be taken at ₹2,88,29,460 for computation of long-term capital gain”.

When Mehrishi’s authorised representative (AR )was asked about this discrepancy, he submitted an amended sale deed dated July 15, 2014. This stated that the conversion of land—mentioned in the 2013 sale deed and which was primarily meant for agricultural purposes—stood cancelled by the competent authority since Mehrishi (the seller) hadn’t deposited the requisite fees for the conversion of the land.

Mehrishi’s AR stated: “…since the Assessee did not deposit the required charges for conversion of land for the interim/generally approval for conversion of land, which got automatically cancelled/lapsed on June 12, 2013, before the transfer of the land.” Hence, the land still stood as agricultural land.

But the IT department rejected Mehrishi’s plea, maintaining that Mehrishi knew the nature of the property before it was sold. Its assessment order stated: “Thus, there are two contradicting deeds on record in respect to nature of land whether the land is agricultural or not.”

Keeping in mind these contradictory statements, the IT department called upon the sub-registrar of Amer on December 20, 2016, to clarify whether the land sold in November 2013 by Mehrishi was agriculture land or commercial land as per the date of sale.

On December 23, 2016, the sub-registrar sent the IT department a letter stating that the valuation of the land has been made in the following manner: “13.794 square yards of the land was considered for valuation as residential, while the remaining 0.48 Bigha of land was considered agricultural. The former was valued @Rs 2090 per square yard which is the effective DLC rate as on date of registration of sale deed. By applying this rate, the sub-registrar valued the DLC price of the land @Rs 2,88, 29,460. Likewise, the 0.48 Bigha of agricultural land was valued at Rs 12,94,099 (@Rs 26, 96,040 per Bigha). In this manner, the total value of the property was valued at Rs 3,01,23,560 and stamp duty was charged accordingly.”

Basically, this is how the scenario played out. The land-use of the 1.26-hectare land located at Gunawata village was first converted by Mehrishi in 2012 from agricultural to non-agricultural. It was sold in 2013 at the rate of non-agricultural land, which fetches a higher market price. Mehrishi did not pay the requisite fees for the change in land-use before the land was transferred to the buyer in 2013. And so the land-use was not converted to non-agricultural but remained as agricultural land on paper. While filing his income tax returns for 2014-15, Mehrishi showed the land as being agricultural in nature—which exempted him from being taxed on it.

The tax department also established that the buyer of the said property had deducted tax at source at one per cent of the total sale value—which is only applicable on transfer of non-agricultural land. So the transaction was within the definition of a “capital asset” because, at the time of sale, the buyer of the property had deducted this tax at source. The IT department’s assessment order said: “An amount of ₹2,50,000 was made as TDS by the buyer of the property and assessee has claimed the credit of this amount in his return of income.”

According to Income Tax rules, the TDS provision is applicable on the transfer of certain immovable properties other than agriculture land. Keeping this in mind, the IT department raised this point: “If it was agriculture land then there was no need to get tax deducted by the buyer of the property and the assessee should not agree upon with the buyer for TDS.”

In its assessment order, the IT department also said: “…it is amply evident and clear that the Assessee transferred agricultural land on 21.11.2013 and does not fall within the definition of Capital Asset U/s 2(14) of the Income-tax Act, 1961 and no capital gain is charged on such transfer.”

Finally, the IT department said Mehrishi had deliberately delayed his tax return filing—being a salaried person, he was supposed to file his income tax returns by July 31, 2014, but he skipped the last date because he was not sure of the tax treatment on this particular land deal. The IT assessment order said: “He (Rajiv Mehrishi) did not file within that time frame and filed the return of income on October 27, 2014, which shows assesse [sic] himself was not sure about the tax treatment of sale of land”.

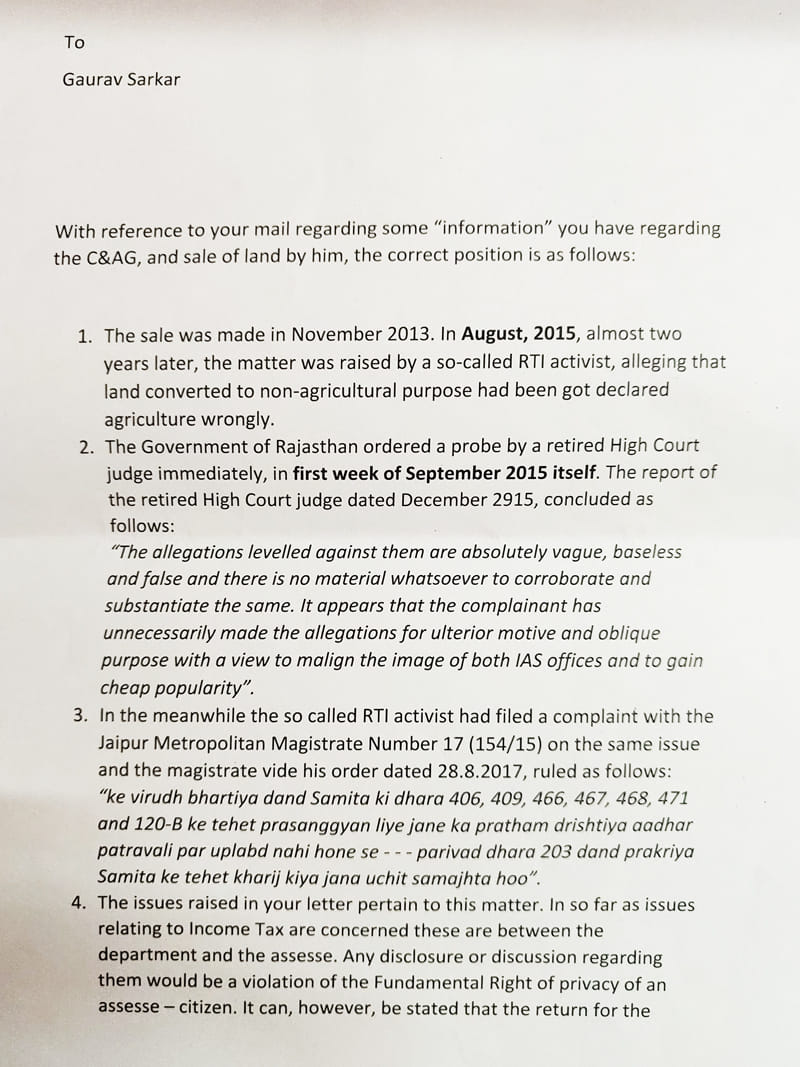

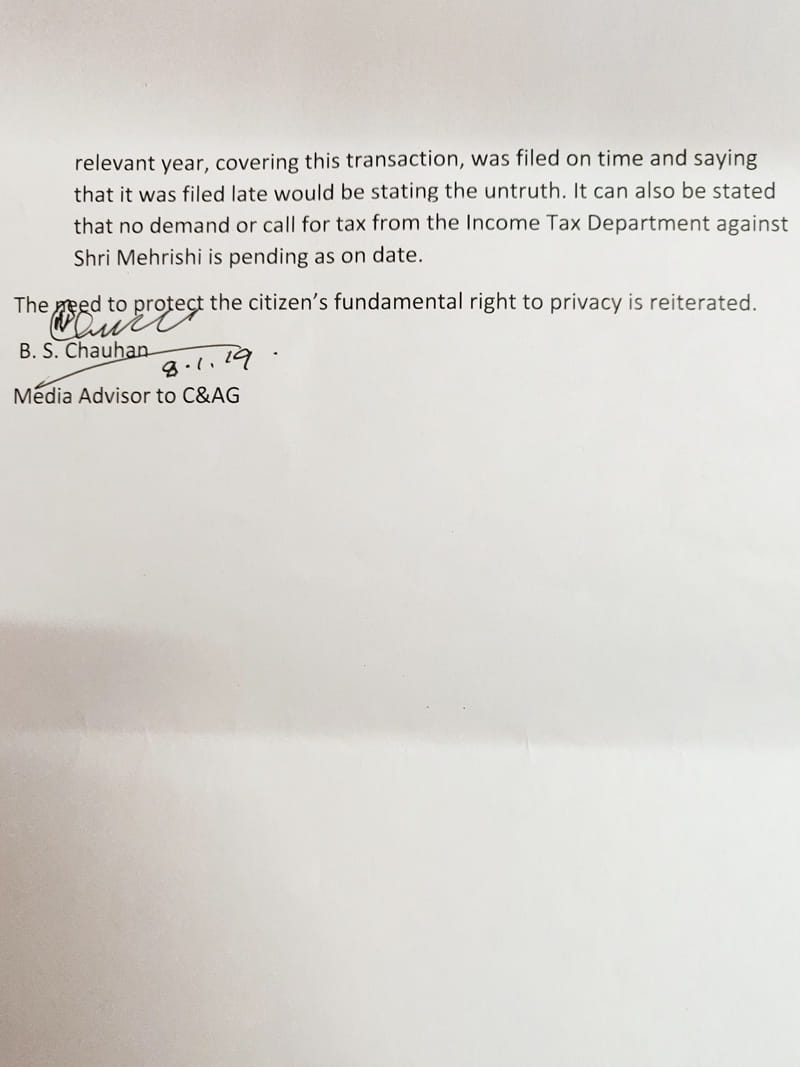

Newslaundry reached out to Rajiv Mehrishi’s office for comment. Here are excerpts from the response we received: “In so far as issues relating to Income Tax are concerned, these are between the department and the assessed. Any disclosure or discussion regarding them would be a violation of the Fundamental Right of privacy of an assessee-citizen. It can, however, be stated that the return for the relevant year, covering this transaction, was filed on time and saying that it was filed late would be stating the untruth. It can also be stated that no demand or call for tax from the Income Tax Department against Shri Mehrishi is pending as on date.”