NL SENA

India’s unreal estate: Why you still can’t afford to buy that home

Are you wondering if home prices will fall in the post-Covid world? There’s something you should know: the real estate industry in India doesn’t want this to happen.

The film director Basu Chatterjee who recently died was known for making slice-of-life cinema. Among his lesser known movies is a movie called Kirayadar (tenant) which was released in 1986. Showing the travails of renting a house in a big city like Mumbai, it’s one of the few Hindi movies based on the story of a tenant and the struggle with the landlord. Also, the title song of the movie, more than the movie itself, is a wonderful summary of all the problems that a tenant has to face.

In fact, from putting up a huge security deposit to dealing with huge insecurities and egos of landlords (simply because they happen to own a house and nothing more), and neighbours who don’t treat you well because you are a tenant, tenants in India have to go through a lot. On top of all this is the massive pressure from parents and relatives to get “settled” in life by buying a house.

Of course, there is some flip side to this as well, with tenants making life difficult for landlords by not moving out once the contract ends or creating a general nuisance.

The trouble is that in most Indian cities, home prices went up at a massive pace between 2002 and 2015. And even though they have fallen in a few places and remained stable in others, home prices still remain unaffordable for the average Indian.

The question I have often been asked over the last decade is, when will home prices fall? If one goes by basic economics and the law of demand, home prices should have fallen dramatically by now. But they haven’t. The reason for this, as we shall see, is that real estate in India has become a low supply, low demand market (yes, low demand — you read that right).

How will things play out in the post-Covid environment? There is bound to be some fall in home prices. But will that be enough to get buyers back into the market? Not immediately, simply because the fall in prices won’t be enough to draw in buyers, especially at a time when people are losing jobs, incomes are falling or stagnating, and many small-businesses are collapsing.

And more than anything, there is a whole system out there, the deep state of real estate in India, which does not want home prices to fall.

The great Indian slowdown

Biscuits sold well under the Lockdown. Parle G, one of the most popular biscuit brands in the country, achieved its highest sales volumes in eight decades between March to May 2020.

It seems biscuits were very popular with the thousands of migrant labourers who walked to their homes from India’s biggest cities. Those stuck at home, thanks to the lockdown, and looking to snack also ate more biscuits than they normally would.

In fact, biscuit sales might just prove to be the exception to the rule when it comes to businesses and the economy this year. The rating agency Crisil expects the total revenues of the fast-moving consumer goods, or FMCG, sector to fall 2-3 percent (or what the analysts like to call “de-grow”) during this financial year. Before Covid-19 struck, the revenues of these companies were expected to grow by 8-10 percent.

FMCG companies produce products of everyday use, everything from soaps to detergents to toothpaste to shampoo to packaged food to beverages. Typically, the sales of these companies are expected to be the most stable of the lot. The reason for this is really simple; come what may, people will continue to buy products of everyday consumption. This logic stems from the fact that people will bathe regularly, wash clothes regularly, brush their teeth regularly, eat regularly, and so on.

But Crisil expects the sales of these products of everyday use to contract this year. One of the major reasons for this is the fact that the incomes of many individuals are expected to fall during the course of this year. In an environment of falling income, people look to cut down on even their everyday expenses.

When people are cutting down (or not increasing, even) their everyday expenditure, it means that things are rather desperate on the income front. In this environment, expecting them to buy what economists like to call “discretionary products” is rather low. Discretionary spending includes money spent by people on everything beyond food, toiletries, clothes, fuel, etc. This includes automobiles, electronics, and even homes.

When people are not confident about their economic future, as the situation is currently, they don’t like buying big-ticket items (like an expensive TV or an expensive mobile phone or an air conditioner or a washing machine, etc.), or committing to make a downpayment out of their savings (in the case of buying a car or a home) or committing to repaying an EMI for a period of a few months or many years (in the case of buying pretty much anything these days).

In this context, it is very interesting to see what RC Bhargava, the chairman of Maruti Suzuki, the country’s largest car maker, had to say to Business Standard. Bhargava was confident that Maruti will be able to sell what it produces in the month of June. This confidence comes from the fact that the company will end up assembling only 30-40 percent of its cars in comparison to what it normally produces in June.

The reason for this lies in the fact that the Maruti is basically an assembler of cars now and depends totally on its vendors and suppliers for everything that goes into the making of a car. And until these vendors and suppliers come out of the lockdown-related issues that they are facing (from a shortage of labour to a breakdown in supply chains), the car maker cannot produce as many cars as it used to.

Given this, Bhargava remains confident of selling the cars that Maruti will produce in June and July. Nevertheless, as Business Standard points out: “[Bhargava] however, added he could not predict the scenario after July, and whether the current trend was merely ‘pent-up demand’ after the lockdown.”

While Bhargava hasn’t said anything outright, it doesn’t take rocket science to conclude that the June and July sales of cars will basically be pent-up demand for the lack of sales between the last week of March and the end of May. Let’s take a look at Figure 1 which basically plots the growth and fall in domestic car sales over the last five years.

Domestic car sales have fallen every month from November 2018 onwards, in comparison to a year earlier. The same is also true for two-wheelers, with sales having fallen every month from December 2018 onwards. The growth and fall in two-wheeler sales over the last five years is plotted in Figure 2.

In fact, two-wheeler sales fell by 16 percent and 20 percent respectively in January and February 2020. It is worth remembering that this was the period before the negative impact of Covid-19 started spreading through the Indian economy.

What this tells us is that the Indian consumer was going slow on purchasing both cars and two-wheelers even before Covid-19 struck. This will only worsen in the time to come as the negative impact of Covid-19 spreads further.

India was already going through a period of economic slowdown before March 2020. In 2020-21, the overall Indian economy is expected to contract in size.

The economic contraction of 2020-2021

Recently, Shaktikanta Das, the governor of the Reserve Bank of India, or RBI, said: “[The] GDP growth in 2020-21 is estimated to remain in negative territory.” GDP, or gross domestic product, is a measure of the economic size of a country.

When Das said that GDP growth will remain in negative territory during this financial year, what he meant was that the size of the Indian economy will basically contract. It will be smaller than it was in 2019-20.

If Das turns out to be right, as he is more than likely to be, this is the first time the Indian economy will contract since 1979-80, when the economy had contracted by 5.24 percent. This was the year of the second oil shock when, due to a revolution and regime change in Iran, oil prices had gone through the roof and impacted economic growth negatively all across the world.

In fact, in the last six decades, this is only the fifth time that the Indian economy will contract during the course of a financial year. The other four times were between 1960-61 and 1979-80.

While Das did not specify by how much the RBI expects the Indian economy to contract in 2020-21, the World Bank expects the Indian economy to contract by 3.2 percent. As per the economists at Goldman Sachs and Nomura, the Indian economy is likely to contract by five percent in 2020-21. Economists at Bernstein expect the Indian economy to contract by seven percent. The Organisation for Economic Co-operation and Development, or OECD, expects the Indian economy to contract by 7.3 percent in 2020-21.

Of course, one of the reasons for the contraction in the economy will be the fact that Indians will cut down on consumption in 2020-21. This includes buying fewer cars and two-wheelers during the course of this year, despite a likely bump in monthly demand in June and July (in comparison to May).

Dear reader, by now you must be wondering why am I talking about cars and two-wheelers in a piece which clearly has the word “home” in its title. Allow me to explain. I was just trying to establish that the Indian consumer will go slow on big-ticket purchasing during the course of this year.

In a scenario where he is likely to go slow on buying cars and two-wheelers, how likely is he to buy a home is a question well worth asking. Buying a home would require making a downpayment, taking on a home loan (in most cases) and, in some cases, requiring enough money to pay out a part of the transaction in black.

Take a look at Table 1, which basically has the details of the total home loans disbursed by public sector banks and housing finance companies.

The average home loan size in 2016-17, 2017-18 and 2018-19 was Rs 9.03 lakh, Rs 7.83 lakh and Rs 11.83 lakh, respectively. For people living in cities, the average home loan size might appear to be too small. And that’s because of the fact that the bulk of the home loans given by public sector banks and housing finance companies are up to Rs 10 lakh. The trouble is that nothing can be bought in a city with that kind of a home loan.

Table 2 lists the details of loans of up to Rs 10 lakh.

In 2018-19, the average home loan size for a home loan of less than Rs 10 lakh was Rs 2.97 lakh.

One reason that holds back public sector banks from lending to this segment is the especially high rate of default, particularly when it concerns home loans of up to Rs 2 lakh. In 2018-19, the rate of default for loans of up to Rs 2 lakh stood at 20.1 percent. The rate of default for loans between Rs 2 lakh and Rs 5 lakh stood at 3.6 percent, much lower than the rate of default for loans of up to Rs 2 lakh, but significantly higher than the overall rate.

While home loans of less than Rs 10 lakh form a significant proportion of the loans given by public sector banks and housing finance companies in numerical terms, in value terms, they aren’t really big. In 2018-19, these loans formed around 36 percent of the number of home loans given, but in value terms, they formed just nine percent of the overall loans.

When it comes to actual disbursements, the major part of the disbursements (in value terms) was for loans of more than Rs 25 lakh. In 2018-19, loans of greater than Rs 25 lakh formed 62 percent of the overall home loan disbursements carried out by public sector banks and housing finance companies.

This is what we will concentrate on in this piece. The average loan size of loans greater than Rs 25 lakh in 2018-19 was Rs 28.68 lakh. Of course, the data here includes only home loans given out by public sector banks and housing finance companies.

Over and above this, private banks also give out home loans. The National Housing Bank does not take their data into account. A July 2018 newsreport in the Mint points out that the average home loan size for ICICI Bank was at Rs 30 lakh. So, the size of the average home loan given by private banks is generally slightly higher than that of public sector banks. But that doesn’t really change the logic of what I am about to say.

What kind of a home can a borrower hope to buy if he takes on a home loan of this size? The median loan-to-value ratio of public sector banks as of March 2019 was 69.9 percent. For housing finance companies, this was at 72 percent. We can roughly say that financial institutions financed around 70 percent of the official price of the house by giving a home loan.

This meant that the borrower had to bring in 30 percent as downpayment. On a loan of Rs 28.68 lakh — the average loan given by public sector banks and housing finance companies in 2018-19 — the downpayment works out to around Rs 12.29 lakh. Hence, the official price of the house works out to around Rs 41 lakh. If there is a black component involved, that is over and above this.

It needs to be mentioned here that we are looking at data as of March 2019. The latest data in this case isn’t available. But what is available is the RBI House Price Index which suggests that home prices went up by three percent between December 2018 and December 2019. We can assume the same house price increase between March 2019 and March 2020.

This means that the official price of such a house as of March 2020 would have been around Rs 42.2 lakh (1.03 multiplied by Rs 41 lakh). The question is, will the Indian consumer buy this house in the post-Covid environment by taking on a home loan?

Why have people gone slow on buying homes?

In an environment where even the FMCG sector is expected to contract, and car sales and two-wheeler sales have already gone down, it is very difficult to see people queuing up to buy homes to live in. The financial commitment required for this in an environment where jobs are being lost and incomes are going down is just too much. (Of course, the example I have used is an average, but the logic applies to the economy as a whole.)

The trouble with the residential real estate sector in India is that there is very little agglomerated data going around, which would help us understand broad trends. But we can draw inferences from the data we have available.

Let’s take a look at the growth in incremental home loans of banks over the years. In Table 1 and Table 2, we looked at home loans disbursed. Along with home loans being disbursed every year, they are also being repaid. Once we adjust for that repayment, what remains are the incremental home loans. In Figure 3, we plot the growth of incremental home loans for banks. Banks control around two-thirds of the home loan market.

There is another chart that suggests precisely this. Take a look at Figure 4.

Figure 4 plots the returns on housing as per the RBI’s House Price Index. These are all-India returns which are made up from returns from specific cities (Ahmedabad, Bengaluru, Chennai, Delhi, Jaipur, Kanpur, Kochi, Kolkata, Lucknow and Mumbai).

It is entirely possible that the returns you made from real estate might have been more than what the chart shows — or even less, for that matter. Also, the chart plots one-year returns starting from December 2011, and it plots yearly returns every three months over the last nine years. This is a weakness in the chart, given that real estate started rallying post 2002 and actually rallied the most between 2002 and 2011.

This is why the one-year all-India return in December 2011 stood at 26.3 percent. In fact, returns in some cities were even higher. The one-year return in Delhi in December 2011 stood at 48.4 percent. In Bengaluru, the return stood at 41.6 percent. But what takes the cake is the one-year return in Kolkata in December 2012 and March 2013, which stood at a whopping 57.5 percent and 59.7 percent, respectively. Those were the days.

In fact, as we shall see, such astonishingly high returns still have some role to play in the currently dysfunctional real estate market in India. While the specifics may vary across India, Figure 4 does show a broader trend. Housing price growth over the last nine years has slowed down big time. The all-India yearly return on housing in December 2019 stood at just 3.5 percent. A bank savings account could have possibly paid you more. The five-year return on housing works out to just 6.7 percent per year. Fixed deposits would have paid more with considerably less risk.

Also, it needs to be pointed out here that the return on housing discussed above doesn’t really take into account the various expenses of owning a home. These include maintenance charges to the society, general maintenance charges, property tax, interest to be paid on the home loan and, above all, inflation.

There are tax benefits of owning a house by financing it through a home loan. Also, one can rent a home out and earn money from it, though it needs to be said here that the rental yield (annual rent divided by the market price of the house) in most parts of the country is between 1.5-2 percent, which is very low.

Once we take all these factors into account, the return on owning a house over the last few years may even be in negative territory. This explains why the so-called real estate investor is nowhere as active as he used to be a decade ago. And that, in turn, is also one of the reasons for the huge amount of unsold inventory of homes that builders have been stuck with over the years. There are multiple estimates of this, depending on which real estate consultant one wants to believe.

As per Proptiger.com , the nine major residential markets in India had a total unsold inventory of 7.75 lakh units as of December 2019. Of this, nearly 3.90 lakh units were in the affordable segment. Another estimate made by property consultant JLL suggests that the number of unsold homes across the top seven property markets in the country was 4.55 lakh units as of March 2020. This unsold inventory was worth Rs 3.7 lakh crore.

An October 2019 report by Liases Foras, a real estate research and consultancy firm, had pointed out that the total number of unsold homes across India was over 13 lakh units. These homes were supposed to be worth a huge Rs 9.38 lakh crore.

Over and above this, there is a huge number of homes that have been bought as an investment over the years and are lying locked, because the landlords are not comfortable with the risk of renting these homes out. In fact, Anshuman Magazine of the property consultancy firm CBRE had said five years back that "around 12 million completed houses" were "lying vacant across urban India".

So, the total number of unused homes — homes that have been built, but with no one living in them — is pretty huge. And a home in which no one lives is largely a waste.

What this clearly tells us is that an astonishingly high amount of money is stuck in real estate, which is not a good thing in a capital deficient country like India. Also, unless these homes get sold, loans given by banks and NBFCs will continue to remain stuck.

Other than the real estate investors disappearing, the major reason for such a huge amount of unsold homes is the price of these homes. It is beyond what most people who actually want a home to live in can afford.

Between December 2010 and December 2019, home prices across India rose by 12.1 percent per year. But as mentioned earlier, this does not take into account the massive increase in home prices before that, between 2002 and 2011. In fact, prices in Delhi, Mumbai and other cities rose by even more than 25 percent in a year in many of these years. This growth continued well into 2015. The one-year housing return in March 2015 stood at 17.5 percent.

The point being that even though the increase in housing price has slowed down since 2015, the base price of homes was already very high by then, making homes unaffordable for most people looking to buy one to live in.

And that explains such a massive rise in the inventory of unsold homes.

Why don’t home prices fall?

Home prices need to come down for homes to become affordable. Even the so-called affordable homes aren’t really affordable. If they were, they wouldn’t have seen such a massive pile up of inventory, as has been the case.

The question is, why don’t home prices fall? The answer to this is a rather complicated one and there are several reasons for the same. Let’s look at this in detail.

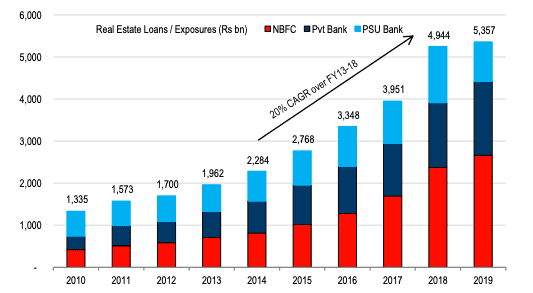

Take a look at Figure 5. It basically plots the total amount of money lent by banks and non-banking finance companies (NBFCs, including housing finance companies) to real estate companies.

It is interesting to see that the total amount of money lent to real estate companies by banks and NBFCs has gone up dramatically over the years, with a bulk of this increase coming after 2016.

The overall bank lending to real estate companies increased from Rs 1.78 lakh crore as of March 2016 to Rs 2.3 lakh crore as of March 2020. This means an increase of 6.6 percent per year. This was much slower than the increase in non-food credit by economic activity, which was at 8.9 percent per year during the same period.

The Food Corporation of India and other state procurement agencies buy rice and wheat directly from the farmers across large parts of the country at a minimum support price decided by the government. Banks finance this purchase. This is referred to as food credit. Once this is deducted from the total loans given by banks, what remains is non-food credit.

So, the bank credit to the real estate sector has grown at a fairly conservative pace over the last few years. In fact, a bulk of the growth in bank lending to real estate came between 2007-08 and 2012-13, when the overall lending grew from Rs 63,168 crore to Rs 1.26 lakh crore, at a rate of 14.8 percent per year.

What this means is that the lending by NBFCs to real estate companies has grown rapidly in the last few years. Why has that happened? Take a look at Figure 6, which basically plots the total amount of lending carried out by banks to NBFCs.

As can be seen from Figure 6, the lending by banks to NBFCs started going up only post December 2016. Why is that the case? In November 2016, the government demonetised notes of Rs 500 and Rs 1,000. These notes had to be deposited with banks. Banks suddenly saw a huge inflow of deposits, without a similar increase in loans. Banks then started increasing their lending to NBFCs which, in turn, lent a lot of this incoming money to real estate companies.

How is all this related to real estate prices not falling? The business model of real estate funding has changed over the years. In the past, real estate companies would launch projects and sell under-construction property. This money would then be used to either buy land or complete a previous project or simply be siphoned off. Another project would be launched to raise money in order to build or complete a project that had been announced in the past.

If I were to talk like an analyst, real estate companies were in a negative working capital business. They didn’t have to put their own money into the business upfront. This model broke down once many builders became too cavalier in their approach and did not deliver apartments on time. This started happening around 2009 and peaked a few years later. Other than genuine buyers, investors also got caught in this scam (for the lack of a better word).

Hence, the model of launching a project and funding a previous project basically broke down. Gradually, under-construction property was looked down upon and real estate companies had to start depending on more formal sources of finance. Their very own little Ponzi scheme, where they raised money from a new project to finance a past project, basically broke down.

Also, after letting the sector run riot for many years, the government finally decided to regulate it. With the passage of the Real Estate (Regulation and Development) Act, 2016, real estate companies need to have all approvals in place before the launch, unlike previously, where they used to launch projects with barely any preparation. Hence, real estate companies need to have all the approvals in place before they start selling the project. This means they need to invest money upfront.

As Arvind Subramanian and Josh Felman write in a paper titledIndia’s Great Slowdown: What Happened? What’s the Way Out? : “Historically the bulk of formal sector real estate funding was provided by banks, but in recent years most of the incremental lending has come from NBFCs, so much so that by 2018-19, NBFCs accounted for about half of the Rs 5 lakh crore in real estate loans outstanding. This funding was provided on the assumption that developers would be able to complete their projects, sell off their inventories, and then repay.”

But as we know inventories have only gone up over the last few years. This basically means that builders already had a lot of unsold homes. On top of that, they built more homes and sold fewer homes than the new homes they have built. This led to the inventory going up.

As Subramanian and Felman write: “In terms of the number of units, unsold inventory in the top eight cities has risen to nearly 10 lakhs at end-June 2019, compared to annual sales of just over two lakh units. Translated into rupees, unsold inventory amounts to Rs 8 lakh crores, equivalent to around four years’ worth of sales.”

As we have seen from data provided earlier, the inventory situation has only become worse since June 2019. So, why haven’t real estate companies cut prices and brought down their inventory? As Subramanian and Felman point out: “While developers could in principle tempt buyers into the market by reducing prices, they couldn’t do this in practice because lower prices would have destroyed the (notional) value of the collateral that they had pledged in order to secure their lending.”

When builders borrowed money from banks and NBFCs, they had to provide collateral for the same. The collateral came in the form of the homes they had built and not sold. In that scenario, if they cut prices and sold homes, the value of the collateral would fall. This would create a problem both for real estate companies and banks. This is why they ended up with a huge unsold inventory along with unreal prices which most genuine buyers cannot afford.

What about individual buyers who bought flats over the years as an investment and continue to hold on to it, unwilling to sell it at a lower price? Buyers who bought flats late in the day, between 2012 and 2015, paid a high price for what they had bought. After factoring in the costs of owning real estate, they may feel they have barely made any money from their investment.

They are holding on to their investment in the hope and the belief that someday, the good days of the past will return, and they will make good money from their investment. Meanwhile, they seem to be ready to hold on to what is basically a losing investment.

In some other cases, buyers are anchored on to the prices they saw before 2015. While, on the whole, the Indian real estate market has generated positive though minimal returns even after 2015, there are parts of the country where real estate prices have gone down.

Meanwhile, this has created a situation which is rarely seen in any economic system. There is low demand for real estate (given the high price) and there is low supply as well (given that real estate companies and individual owners are unwilling to cut prices). I may want to buy a home but unless I have enough money and the ability to borrow to do so, I am really not adding to demand. Just wanting something, without having the money to finance it, doesn’t really add to demand.

There are other reasons also as to why transactions are not happening.

In some real estate markets, the market price is lower than the prevailing circle rate. What does this mean? State governments decide on a certain circle rate for different areas. If a real estate transaction happens, then stamp duty needs to be paid on this rate, irrespective of the prevailing market price. When the market price is higher than the circle rate, there are no problems.

But when the market price goes below the circle rate, it creates multiple problems. Let’s say the market price of a particular apartment in a city is Rs 50 lakh. The circle rate is Rs 60 lakh. If this apartment is sold, the stamp duty will have to be paid at the circle rate of Rs 60 lakh and not the market price of Rs 50 lakh.

Also, Rs 10 lakh — the difference between the circle rate and the market price — will be added to the buyer’s income and he will have to pay income tax on it. On the seller’s side, the capital gains will be calculated using a selling price of Rs 60 lakh and not Rs 50 lakh. This is done to discourage black transactions.

This basically ensures that real estate transactions in such markets don’t happen at all. This means that the inventory with real estate companies does not come down. Along with this, the individual buyers also cannot sell the apartments they own. There is a clear need on the part of the state governments to ensure that the circle rates are at realistic levels.

The question is, why don’t state governments decrease circle rates to realistic levels? One reason for this can possibly lie in the fact that most of the ill-gotten wealth of state-level politicians is in real estate. In fact, many real estate companies, both small and big, are essentially fronts for politicians. A decrease in circle rates would mean that transactions will start happening at a lower price. This is something that politicians don’t want because it will mean a decrease in their overall wealth. They would rather have no transactions than have transactions at a lower price. Do remember, all these investments are in black.

Then there is also the case of stamp duty on real estate transactions forming a significant portion of the revenue of state governments. While at lower stamp duty rates, the chances of more real estate transactions are higher, this is a risk that state governments don’t seem to be willing to take. Take a look at Table 3, which lists out the stamp duty collections of a few states.

Will home prices fall in the post-covid world?

What we have discussed up until now are reasons from the past. The question is, how will things evolve in a post-Covid world? Will real estate prices fall?

Let me put it this way, before I get into the details: the deep state of Indian real estate that prevails (the real estate companies, the real estate consultancies, the governments, the banks, the investors and the NBFCs) will try their best to ensure that real estate prices do not fall.

The mathematics of the entire business works out such that builders currently cannot cut prices by more than 5-10 percent. Analyst Adhidev Chattopadhyay pointed this out in a recent report he wrote for ICICI Securities. The logic for central and south Mumbai, where the country's most expensive real estate is sold, is slightly different.

What did Chattopadhyay say? Let’s look at it pointwise.

- The gross margins that real estate companies work with are around 15-20 percent. This is for non-Mumbai real estate companies operating in the biggest cities in the country. The average selling price is Rs 5,000-6,000 per square foot and has been stagnant post demonetisation. If we take construction costs, approval costs, land costs and marketing costs, this works out in the range of Rs 4,300-4,900 per square foot. What this implies is that there is a very limited scope for real estate companies to cut prices in order to make their homes attractive enough for prospective buyers.

- Unlike manufacturing companies, the cost of building homes varies across different parts of the country. Also, money in building homes is spent over a period of four to five years; hence, costs cannot suddenly be brought down. In this scenario, it will be difficult for real estate companies to cut prices beyond 5-10 percent (again non-Mumbai). If they go beyond that, they will need to make loss-making sales and no one wants to sell at a loss. This means stagnation in the market and the low supply, low demand scenario that I had talked about earlier.

Chattopadhyay also feels that these price cuts will be more along the lines of indirect discounts from real estate companies, rather than a direct cut in the market price. The reason for this is very straightforward. No real estate company is able to sell all the homes that it builds in a particular project all at once. The initial sales happen at a certain price. If the real estate company cuts prices in the days to come, this does not go down well with the individuals who had bought these homes at the beginning. Hence, the pricing remains opaque and discounts need to be negotiated.

Over the long term, this has been a major reason why real estate in India has become sluggish. There is nothing like a market price. On the flip side, what this tells any prospective buyer is to negotiate hard. It might just be your lucky day.

- In the days to come, labour costs are unlikely to come down. Many construction workers have gone back to their homes in states like Bihar, Uttar Pradesh, Jharkhand, Odisha, Chhattisgarh, etc. Given this, there will be a shortage of construction workers. Hence, the wages paid to labourers will go up, driving up the cost along the way.

Over the years, a lot of foreign money has come into Indian real estate (particularly commercial real estate). Analysts who track real estate expect the money coming in through this route to slow down in the time to come. Most of this money came in from Western economies. And now that these economies are in a recession, the money coming in is bound to slow down.

The problem with this argument is that an equally convincing and opposite argument can be made. Take the case of the United States. Between February 26 and June 10, the Federal Reserve, the American central bank, printed a little over $3 trillion. Other Western economies are also printing money. This money can easily flow to any part of the world. Of course, whether it does remains to be seen.

Kunal Lakhan, an analyst at CLSA, makes a very interesting point regarding all the inventory that has piled up in central Mumbai (the areas of Dadar, Prabhadevi, Worli, Lower Parel, Parel, etc.). Lakhan says that there are 3,000 apartments in this area, with an average price of Rs 10 crore. The question is, who is going to buy these homes? There are 3,780 multi-millionaires in Mumbai. Most of these individuals already have homes in south Mumbai (which has the country’s most expensive real estate). So, how many more homes can they buy?

Lakhan estimates that some of the key projects in central Mumbai have seen a fall in price of 25-30 percent within one or two years of getting the occupation certificate. He estimates that prices might fall a further 12-15 percent in the post-Covid environment in case of some projects. The inventory piled up could take up to a decade to clear. There is a ghost city right in the middle of Mumbai. It’s just that it can’t be seen (like Greater Noida) because it’s all up in the air.

So, when it comes to central Mumbai, the market is at work and the home prices have taken some beating. But the average price of the apartment is still so high that demand has totally collapsed. As I said earlier, if you are the kind who can afford such an apartment, you probably already have one, but if you still want to buy another one, negotiate very hard.

The new new real estate story

The above reasons are genuine. But the fact of the matter is that for any market to work, the price at which consumers are willing to buy should match the price at which suppliers are willing to sell. In the case of real estate, whatever the companies and their lobbies might say, transactions are not going to happen unless home prices come down.

Real estate consultancies and many analysts who follow the sector have now started talking about the economic environment improving by October and the demand coming back.

There is nothing new here. This is something that has been happening for the last five years wherein sometime during the middle of the year, those who make their money from real estate start talking about a festival season boom in the sector. The boom hasn’t come, at least not in the last five years.

Why should this year be any different? If things did not improve during the years when economic growth actually happened, how can they improve during a year when the economy is expected to contract? No real estate analyst worth his salt is willing to answer this question.

If homes weren’t selling before Covid-19 struck, how are they going to sell in the post-Covid economic scenario, where incomes are likely to fall/stagnate, jobs will be lost, and businesses will be destroyed? This is another question that nobody is currently willing to answer.

The real estate industry is trying to sell a positive story all over again. One strand of this story is builders going digital in order to beat the post-Covid economic heat. This essentially involves the real estate company arranging a virtual visit of the home for a prospective buyer. They are also setting up virtual meets for the prospective buyer with banks and home finance companies for a home loan.

While it’s fantastic that companies are resorting to technology in order to boost their sales, I am really not sure about how many people are going to buy a home without going out there and seeing it for themselves. This might help a few big builders with some reputation to sell a few units here and there; nevertheless, it’s not going to help in clearing the massive inventory in any meaningful sort of way.

The other story being sold is that people who are losing their jobs in the Middle East will come back and buy homes to live in. There is a big hole in this argument. A bulk of these people already own homes in India. As a recent report in Mint points out: “Every fifth house in Kerala belongs to a person who works in the Gulf.” So, yes, some of these people may come back and buy homes, but again, this isn’t going to lead to any significant reduction in the inventory.

The big question

How will the real estate companies repay loans they have taken on from banks and NBFCs, if they don’t get around to selling the unsold inventory of homes?

As I had said earlier, the system will come to their rescue and it has. In April earlier this year, the RBI came to the rescue of NBFCs by allowing them to extend by a year the date for starting operations for loans to real estate projects delayed for reasons beyond the control of promoters. This extension won’t be treated as restructuring of the loans given to real estate companies. This facility was already available to banks.

If this extension was treated as restructuring, the banks as well as NBFCs would have to make provisions (that is, set aside money) for a possible default on these loans. And any provision would reduce profit.

This move by the RBI allows real estate companies another year to meet their loan obligations. This helps banks as well as NBFCs in the short term, as the chances of real estate companies defaulting on loans are high, given the lack of new home sales.

As mentioned earlier, quite a lot of what looks like lending to NBFCs on the books of banks is actually indirect lending to the real estate sector. In this scenario, if real estate companies don’t pay up NBFCs, the latter won’t be able to repay banks. Hence, an NBFC crisis might turn into a banking crisis, something the RBI would like to avoid.

The moratorium on repaying principal as well as interest on term-loans is also going to help real estate companies in the short-term. But it is worth remembering that interest is not being waived off on these loans. At the end of the moratorium period, the interest for a period of six months (or three months, depending on the moratorium taken by the real estate company) will be added to the principal outstanding and that will have to be repaid. There is no free lunch available anywhere.

What this basically does is, it pushes the can down the road. The question is, what will happen one year later? Of course, the hope is that demand will come back, real estate companies will be able to sell the inventory they have built up, and use the money to repay loans. As far as hopes go, even cows might fly one day.

Conclusion

If we continue the way we currently are, the real estate sector will continue to stagnate, at least for the next five years, as it has for the last five years. Other than being a huge factor in improving the quality of life that comes with owning a house (children don’t need to change schools, parents are happy, and so on), the real estate sector also has huge forward and backward linkages with 250 ancillary industries.

As Keith Wardrip, Laura Williams and Suzanne Hague write in a research paper titled The Role of Affordable Housing in Creating Jobs and Stimulating Local Economic Development: A Review of the Literature: “During the construction of affordable housing — or any kind of housing, for that matter — the local economy benefits directly from the funds spent on materials, labour, and the like. If the builder is purchasing windows and doors from a local supplier, the supplier may have to spend money on materials and hire additional help to complete the order — examples of indirect effects. Finally, the construction workers, glass cutters and landscapers are likely to spend a portion of their wages at the local grocery store or shopping mall, which illustrates induced effects.”

This basically means that when the real estate sector does well, many other sectors — right from steel and cement to furnishing and paints, etc — do well. The multiplier effect is huge. And the multiplier effect can benefit India currently to tackle the negative impact of Covid and in the years to come.

But for that to happen, home prices need to fall. Hence, it’s time the government and the RBI stop mollycoddling the real estate companies. After the current set of regulatory changes expire, the ones made to help real estate companies when it comes to repaying money they owe to banks and NBFCs, the government and the RBI shouldn’t offer any more help.

Banks and the NBFCs should be allowed to demand repayments and if a real estate company defaults, then the collateral needs to be seized and sold. Real estate companies defaulting on loans need to be put through the Insolvency and Bankruptcy Code.

Of course, this will mean some trouble for banks as well as NBFCs. But they will have to face this trouble sooner or later, given that if the unsold inventory of homes doesn’t get sold, there is no way real estate companies are in a position to repay the loans they have taken on.

In fact, Lakhan of CLSA estimates that the annual debt repayments of the sector are more than twice its disposable income. How is the debt ever going to be repaid if the inventory doesn’t sell?

Also, only once the prices fall, the demand is going to come back, and only then the real estate sector can hope to get back on to its feet.

As Nassim Nicholas Taleb writes in a similar vein in Antifragile in the context of the financial crisis of 2008 and Alan Greenspan, the chairman of the US Federal Reserve between 1988 and 2006: “A main source of the economic crisis that started in 2007 lies in the...attempt by...Alan Greenspan...to iron out the ‘boom-bust cycle’ which caused risks to go hide under the carpet and accumulate there until they blew up the economy.”

The more a government or a central bank tries to postpone a crisis, the bigger the eventual crisis is. This is something that the RBI and the government need to realise.